A margin for error is a norm even in massive operations. However, when a global market is expected to climb to USD 1.76 trillion by 2034 at a CAGR of 18.2%, such a margin for error has effectively vanished.

Hence, in this industry, a single error or “minor bug” might have much larger implications than a simple ticket in the backlog. It can be a direct hit at your reputation and customer confidence, and that is not to mention all the potential regulatory nightmares.

This guide doesn’t aim to give you a fast financial solution, but a way to build secure and scalable financial products. Whether you are a CTO, founder of a disruptive fintech startup, or product owner, and this is exactly what you’re looking for, then this guide is made for you.

Today’s article will be diving into:

- How financial software differs from other general software

- Types of financial systems

- Compliance and security requirements

- Technology stacks, and

- The cost to build financial software.

Key Takeaways:

- Financial software refers to apps that manage and process financial data and transactions for both individuals and organizations.

- Fintech is considered a subset of financial software, a tool used to change the way users interact with money.

- Financial software development is essential for traditional financial institutions, service providers, and even non-financial industries.

- There are 10 different types of financial software, ranging from core banking platforms to insurance software and blockchain-based software.

- The software development cycle of a financial software consists of 7 steps: ideation, architecture and UX/UI design, development, testing, deployment, and maintenance.

- There are multiple regulatory laws that a financial software must adhere to.

- The cost of financial software development depends on the type of product you build and its complexity.

What is financial software development?

Financial software is a category of applications and systems designed to automate, manage, and process financial data and transactions for individuals or organizations. It serves as a central hub for the storage and analysis of fiscal records, ranging from personal budgeting and tax preparation to complex institutional loan management and accounting.

By integrating core features like asset management, business intelligence, and bookkeeping, these tools transform raw data into actionable insights through reporting and visualization.

Beyond mere utility, financial software is defined by its ability to:

- ensure regulatory compliance and

- reduce human error through automation,

- providing a reliable framework for monitoring financial health and

- making informed economic decisions.

Financial engineering is a broad discipline. This guide will focus specifically on:

- Banking and payment platforms

- Lending and insurance systems

- Investment and compliance tools

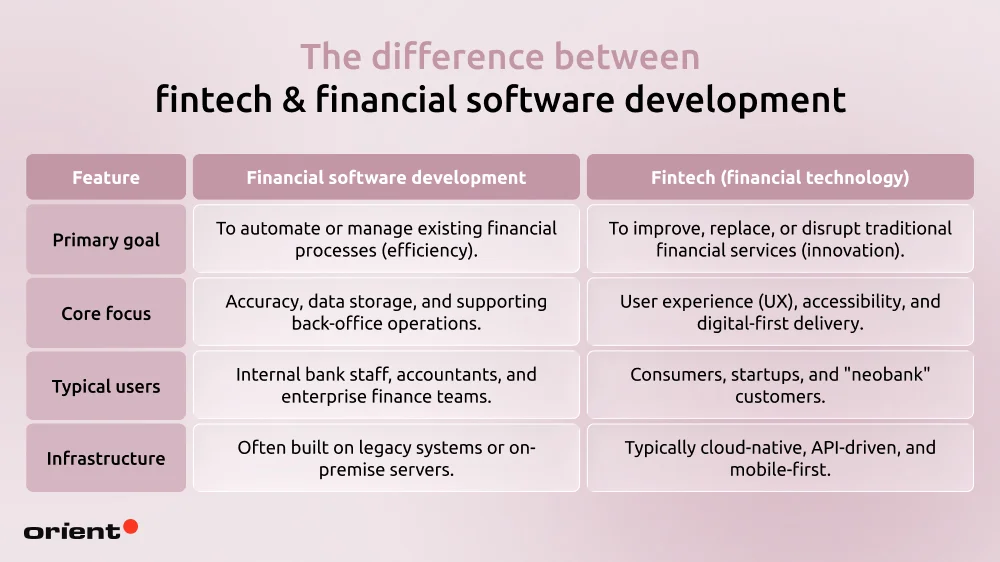

The difference between fintech & financial software development

Fintech, short for financial technology, refers to technology-driven financial services that help businesses and consumers manage financial activities more efficiently through software, algorithms, and digital platforms.

“Fintech” and the phrase “financial software development” might often be used interchangeably, but there are certain differences in their intent and scope.

While financial software is the tool, fintech is the innovation or business model that uses the tool to disrupt or improve the service.

- Financial software has existed since the early days of computing (think of core banking systems that use COBOL in the 1970s), focusing on the utility of the software. This means that a ledger balance or a tax form is calculated correctly.

- A legacy ERP system used by an insurance company to track internal employee payroll is financial software, but it isn’t necessarily fintech.

- Fintech is a modern subset of financial technology. It refers to the use of tech to make financial services more reliable, secure, and inclusive. Fintech relies a lot on modern tech like AI or Open Banking APIs, changing the way people interact with money.

- An app like Robinhood or Revolut is fintech because it uses mobile-first software to disrupt the traditional brokerage and banking industries.

The key differences between the two at a glance are as follows:

Who needs financial software development?

To maintain a competitive edge, multiple industries are looking for custom financial architecture with a diverse range of requirements.

Traditional institutions and fintechs

- Banks and credit unions: These entities require “core banking” modernization to replace aging legacy systems with cloud-native platforms that support mobile banking and real-time processing.

- Investment and brokerage firms: Need high-frequency trading platforms and AI-driven portfolio management tools to provide real-time market insights.

- Lending businesses: Require automated underwriting engines and loan origination systems to speed up credit decisions while managing risk.

Service providers and infrastructure

- Payment processors: They must build high-throughput gateways that handle thousands of transactions per second while maintaining PCI DSS compliance and fraud detection.

- Insurance companies (InsurTech): Need platforms for automated claims processing and risk assessment algorithms that utilize “big data” to personalize premiums.

- Compliance and RegTech: Specialized software is needed to automate KYC and AML checks to prevent fraud and avoid heavy regulatory fines.

Non-financial industries (embedded finance)

- E-commerce and retail: Major retailers now integrate “buy now, pay later” (BNPL) and digital wallets directly into their checkout flow to increase conversion rates and customer lifetime value.

- Telecom companies: Managing millions of subscribers requires complex billing and “mediation” systems that can calculate usage-based charges and roaming fees with zero error.

- Healthcare providers: To maintain cash flow, providers need custom claims management software that automates insurance eligibility verification and reduces the rate of rejected claims.

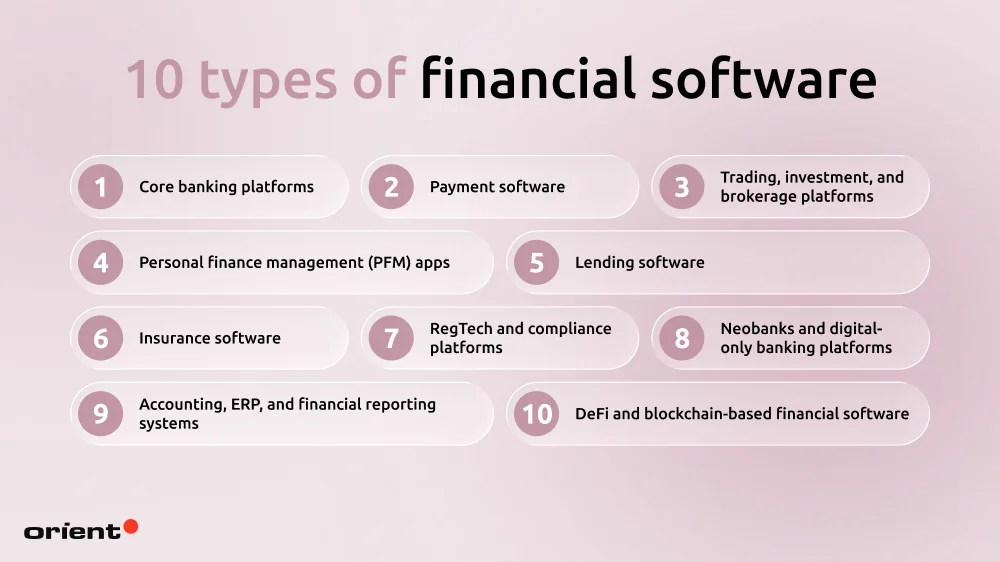

10 types of financial software

Financial software, unlike generic software, is built with high accuracy, strict security, and highly regulated performance. Instead of cramming multiple functions into a single app, different types of apps are built to serve specific operations of the financial sector.

Core banking platforms

Core banking software is the backend system that supports a bank’s daily operations, including managing transactions, customer accounts, and financial records. It handles core banking services such as loans, deposits, mortgages, payments, and customer account management while allowing customers to access banking services across different branches and digital channels.

Core banking systems can also be categorized by their architecture. Three main types are monolithic systems, modular platforms, and cloud-native solutions.

- Monolithic core banking systems centralize all banking functions within a single application.

- Modular core banking platforms break banking functions into separate modules or microservices.

- Cloud-native core banking solutions are built on cloud infrastructure and designed for scalability, flexibility, and faster innovation. They often support technologies like AI, machine learning, and third-party API integrations.

Payment software

Payment software, in the modern financial landscape, refers to the technology that helps businesses process and manage digital transactions securely. It acts as a digital intermediary between the customer’s account and the merchant’s business account.

A payment software is an integrated ecosystem consisting of two components:

- Payment gateway (the frontend): This is the customer-facing “digital terminal”. A payment gateway collects and encrypts sensitive payment data and transmits it to the processor.

- Payment processor (backend): The payment processor operates behind the scenes. After receiving data from the gateway and communicating with card networks and the banks to authorize the movement of funds.

Trading, investment, and brokerage platforms

In the modern financial landscape, the line between trading, investment, and brokerage platforms is continuously blurred. Most users are expecting an integrated experience, but underneath, the architecture usually stays modular and specialized. Here is a quick glance at each type of platform:

- Trading platform: The trading platform is the “cockpit” used by the investor. It sits on top of the brokerage infrastructure and provides the tools needed to execute fast, short-term decisions.

- Investment platform: The investment platform focuses on the “long game.” It often pulls data from the brokerage and trading layers to give the user a high-level view of their wealth and goals.

- Brokerage platform: Think of the brokerage platform as the “back-office engine.” It is the regulated entity that holds the licenses, manages user accounts, and connects to the actual stock exchanges (like the NYSE or NASDAQ).

Personal finance management (PFM) apps

Personal financial management (PFM) software is a type of consumer financial software designed to help users manage their money (this includes income, spending, savings, and investments) to achieve financial stability and life goals. This management is done through features such as budgeting, expense tracking, banking, and bill payments.

In other words, this app acts as your financial manager, tracking and analyzing your spending to provide you with helpful insights and useful financial advice.

Lending software

Lending software is a digital platform that helps banks, lenders, and financial institutions manage the entire loan lifecycle, from application and underwriting to repayment and collections. It automates key lending processes such as borrower onboarding, credit evaluation, risk assessment, document management, payment tracking, compliance checks, and reporting. Modern lending platforms often combine loan origination and loan servicing capabilities into a single system, helping lenders improve efficiency, reduce manual errors, accelerate approvals, and deliver a smoother borrower experience.

Insurance software

InsurTech has seen a significant rise ever since the pandemic, as users are getting used to carrying out every task online. It is a platform that is designed to manage core insurance operations, including policy administration, underwriting, claims processing, and billing. It acts as the operational backbone of an insurance company by supporting the critical workflows and transactions that shape both internal processes and customer experiences.

Some subcategories of insurance software may include:

- Policy management software

- Enterprise risk management (ERM)

- Document management software

- Customer relationship management software (CRM)

- Claim management software

- Underwriting software

RegTech and compliance platforms

RegTech (short for regulatory technology) is a subset of fintech that refers to the use of advanced technologies to help financial institutions manage compliance, monitor regulations, and reduce operational risks more efficiently. By leveraging tools such as big data, automation, and machine learning, RegTech solutions simplify regulatory reporting, strengthen fraud detection, improve data security, and support organizations in meeting constantly evolving financial regulations in a faster and more cost-effective way.

Neobanks and digital-only banking platforms

Neobanks and digital banks are both services in the modern financial world. However, they are quite different and shouldn’t be used interchangeably.

- Neobanks refer to fintech companies that provide digital and mobile solutions for banking services. These companies themselves aren’t licensed banks, so they often partner with one. Neo banks provide a range of solutions and services, such as payment management, budgeting tools, financial analysis, etc. This kind of setup is often referred to as the Banking-as-a-Service (BaaS) model. The licensed back handles the backend, while the neobank company handles the front end and user experiences.

- Digital banks refer to the digitization of traditional banking. In other words, digital banks are backed by traditional banks, offering the same types of services like money deposits, savings account management, financial product application, and more – except customers do not need to visit a physical branch to accomplish these tasks.

Neobanks and digital-only banks reflect the evolution of users’ needs and expectations of fast and convenient 24/7 access to services.

Accounting, ERP, and financial reporting systems

An enterprise resource planning (ERP) system is an integrated software platform that helps organizations manage and streamline core business processes through a centralized system and shared data source. ERP software connects departments such as finance, human resources, fostering operational efficiency.

In ERP, accounting and financing modules handle a range of tasks:

- Cash flow tracking

- General ledger management

- Invoice handling

- Account management, and more.

The ERP provides a consolidated view for financial reporting and accounting systems. Even more crucially, the ERP system provides a routine for automation and analysis. The capability to automate daily tasks and gain insights through critical analysis allows businesses to make confident and data-driven decisions.

DeFi and blockchain-based financial software

Decentralized finance (DeFi) is a blockchain-based financial system that enables individuals and businesses to access financial services directly through peer-to-peer networks, often without relying on traditional intermediaries such as banks, brokerages, or other centralized institutions.

Instead of using fiat currencies and centralized control, DeFi platforms leverage cryptocurrencies, smart contracts, and blockchain technology to support activities such as lending, borrowing, investing, trading, and asset management. By removing many of the restrictions and intermediaries found in conventional financial systems, DeFi aims to create a more open, transparent, and accessible approach to financial services.

Blockchain-based software utilizes decentralized digital ledgers to store data and execute transactions across a distributed network.

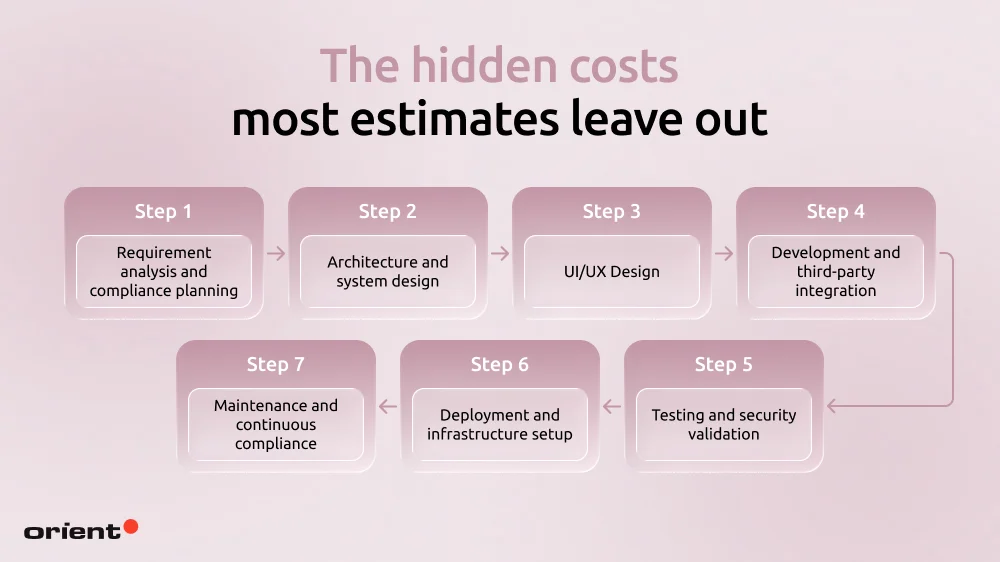

The 7-step financial software development process

Step 1: Requirement analysis and compliance planning

The first step of any software development project is requirement analysis. This is where you answer key questions regarding

- Business and operational goals

- The key compliance requirements, and adjust goals to fit compliance restrictions

- User persona and journey mapping

- Key competitor research

- Edge cases

After having a clear and well-defined scope, the team needs to sit down to plan the most important aspects of the project into an actionable roadmap:

- Timeline and milestones

- Resource allocation and infrastructure provisioning

- Cost estimation

- Risk management and mitigation plans

Step 2: Architecture and system design

Once you have a clear roadmap, it’s time to figure out how the software would survive in a real-world scenario. There are multiple tasks to tackle, but the core ones are as follows:

- Component mapping, communication protocols, and deciding between monolith and microservices.

- Data modeling and API specs (database selection, schema design, API contracts)

- Plan for fault tolerance

- Deciding what kinds of trade-offs you are willing to make, as there are no perfect apps. For example, including heavy encryption in the system will introduce system latency and slow down performance.

Step 3: UI/UX Design

Users have high expectations when it comes to UI and UX. In this stage, the main goal is to turn complex ideas into an intuitive and user-friendly UI.

In other types of apps, the team might be able to focus solely on aesthetics. In a financial app, however, it’s also about creating a UI that is clear and psychologically safe. Key tasks you need to go through to achieve this include:

- Creating wireframes

- Building user flows

- Building interactive user flows to validate the original ideas

- Reducing friction in tasks like identity verification

Step 4: Development and third-party integration

With careful planning and testing, it is finally time to write the code.

During this phase, developers not only build the core logic of the software but also need to ensure that the external APIs are securely connected. To save time building features from scratch, companies often rely on integrating established and compliant third-party services.

Step 5. Testing and security validation

Every app, especially financial apps, must be aggressively tested for bugs and vulnerabilities. After all, real money is put on the line.

Even though we mention testing and security validation as the fifth step, security must be implemented from the very first steps of the project. The key focus during this step often involves functional testing, stress testing, cybersecurity audits, and the assurance of the absolute accuracy of ledger calculations.

Step 6: Deployment and infrastructure setup

At this stage, the primary goal is to deploy the software into a secure and scalable production environment capable of handling real-world traffic reliably.

DevOps engineers configure cloud or on-premise infrastructure to ensure smooth performance and strong system stability. For financial applications, the deployment process must be tightly controlled to minimize risks, prevent downtime, and maintain reliable data backup and recovery strategies.

Step 7: Maintenance and continuous compliance

Deployment is far from the end. To keep the system running smoothly and up-to-date, developers need to constantly perform the following tasks:

- Monitoring the system’s health

- Patching vulnerabilities

- Update code

- Adapt code to match any updates in compliance standards like GDPR or PCI-DSS.

Regulatory compliance in financial software development

The financial world is strictly regulated. These regulations are updated frequently, so it is necessary to keep a close eye on the app’s compliance. Following is a list of 6 key frameworks every financial software needs to adhere to. There might be slight differences depending on one’s specific niche, but the following list is the core ones all financial apps must comply with.

| Framework | What It Covers | Who It Applies To | Key Technical Requirement | Non-Compliance Consequence |

|---|

| GDPR | Personal data privacy and protection of EU citizens. | Any entity processing data of EU residents. | End-to-end encryption, “Right to be forgotten” logic, and 72-hour breach notification systems. | Fines up to €20M or 4% of annual global turnover |

| PCI DSS 4.0.1 | Security of payment card data (Credit/debit). | Anyone who stores, processes, or transmits cardholder data. | Mandatory MFA for all access to card environments; automated, real-time log monitoring; and 30-day critical patching cycles | Fines from $5k to $100k per month; permanent loss of ability to process card payments |

| DORA | Digital operational resilience and ICT risk. | EU financial entities (banks, fintechs) and their 3rd-party tech providers. | Regular “Threat-Led Penetration Testing” (TLPT) and centralized ICT incident reporting architecture | Periodic penalty payments of up to 1% of average daily global turnover |

| AML / KYC | Anti-Money Laundering and Identity Verification. | Banks, Neobanks, Crypto-exchanges, and Payment Processors. | Integration of real-time sanctions screening APIs and automated Suspicious Activity Report (SAR) generation | Heavy fines (e.g., $80M+ recent penalties) and potential criminal liability for executives. |

| PSD3 / PSR | Open Banking security and fraud prevention. | Payment Service Providers (PSPs) and Banks operating in the EU. | Verification of Payee (VOP) to match IBANs with names; enhanced Biometric Strong Customer Authentication (SCA) | Revocation of payment licenses and exclusion from the EU single payment market |

| SOC 2 Type II | Security, Availability, and Data Privacy for SaaS. | Technology service providers and financial SaaS platforms. | Verifiable audit trails for every system access; formal change management workflows for all code deployments | Loss of major enterprise contracts; “untrustworthy” status in the financial ecosystem |

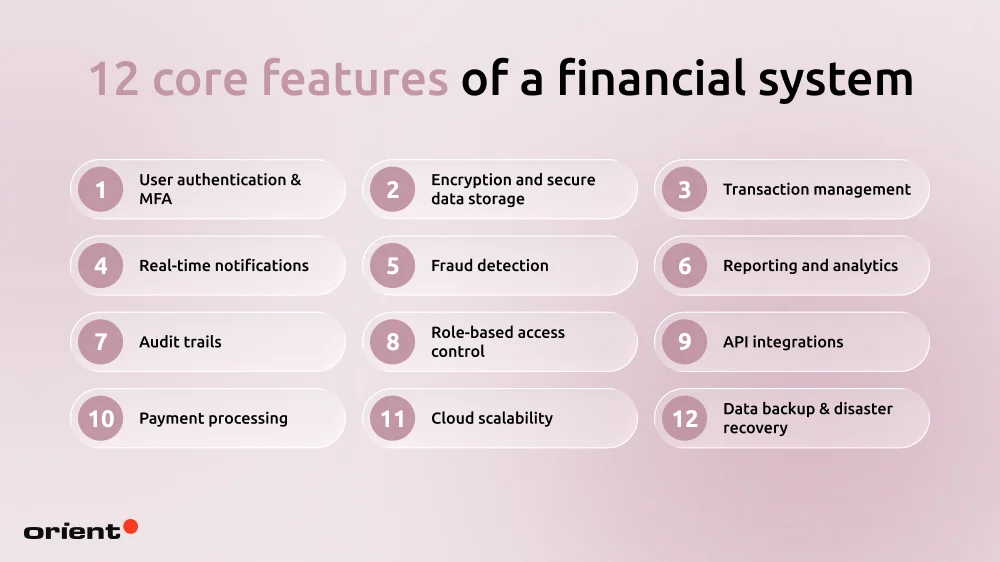

Core features every financial software system needs

User authentication & MFA

The National Cybersecurity Alliance identifies multifactor authentication, or MFA, as a login security technique that necessitates two or more identity verification methods in order to gain access to an account. The password is typically one “factor,” and users can frequently select the other factor. In other words, you should use more than your password to keep the account and data safe, as it is frequently reused across many sites, leaked in data breaches, or even captured by malware.

For all those reasons, financial apps simply can’t afford to skip MFAs. To make MFAs work for your software, you need to take the right approach.

- Implement adaptive MFA based on transaction risk by using contextual data such as location, device, and transaction amount.

- Encrypt sensitive data both in transit and at rest using secure protocols like SSL/TLS, especially for OTPs and authentication data.

- Allow users to choose their preferred MFA method to improve accessibility and user experience.

- Utilize biometric authentication for faster logins and behavioral analytics to detect suspicious activity or anomalies.

- Establish secure fallback and recovery options, such as backup codes or alternative verification methods, for users who lose access to their MFA devices.

Encryption and secure data storage

Encryption converts sensitive data into unreadable code using cryptographic algorithms and keys, helping protect information both when it is stored (“at rest”) and when it is being transmitted (“in transit”).

Following the best encryption practices is how you protect your organization’s and customers’ data:

- Utilize top-tier encryption algorithms: Use AES-256 as your default standard for bulletproof data protection. Pair it with RSA to safely transmit data across the web, or swap in Elliptic Curve Cryptography (ECC) if you need lighter, faster security optimized for mobile and IoT devices.

- Enforce end-to-end encryption (E2EE): Right from the sender’s device, the data will be scrambled and only decrypted when it arrives at its destination. This ensures no one in the middle can peek at the data.

- Defend your data at rest: don’t leave sitting data exposed. Apply full-disk encryption across your hosting servers and go a step further by encrypting highly sensitive individual fields (like social security numbers or banking tokens) directly inside database tables.

- Use secure network protocols: Never send data in the clear. Always wrap network traffic in TLS to prevent wiretapping and data tampering, and mandate HTTPS across all app-to-server communications to block interception attempts.

Transaction management

Transactions are crucial for financial platforms and a primary target for financial crime.

Modern transaction management should transition from retrospective processing to a proactive dual-path architecture.

Key technical pillars for this approach include:

- In-flight authorization vs. streaming analytics: this approach uses fast authorization to evaluate risk and approve or hold transactions in under 100 milliseconds. It also runs contextual machine learning models to update risk profiles, but without adding latency.

- The ingestion stack (Kafka and Flink): Real-time fraud detection depends on powerful stream processing systems that can analyze large volumes of transaction data as it happens. Financial platforms often use tools like Apache Kafka and real-time analytics engines to monitor signals such as location, IP address, and transaction activity, helping identify suspicious behavioral changes.

- Explainable AI for audit readiness: When an anomaly detection system flags or blocks a transaction, teams need to clearly understand why the action was taken instead of relying on a “black box” process. To support compliance and audit readiness, transaction management systems should maintain transparent records and detailed audit logs that help regulators and investigators trace decisions during reviews or fraud investigations.

Real-time notifications

In the finance world, time is money. Every delay costs money, a valuable opportunity, or hurts the compound interest. Provide your users with real-time notifications to keep them updated and give them the chance to act in a timely manner.

Real-time notifications also help protect the account. Immediately flagging suspicious activities or a high-risk transfer allows users to act immediately, before any damage is done. Lastly, it is best to develop behavioral models that continuously adapt over time, rather than relying on rigid, hardcoded thresholds.

Fraud detection

Fraud detection is the process of identifying and preventing suspicious activities that may indicate financial crime, unauthorized access, or other fraudulent behavior. Using a combination of monitoring processes and detection technologies, organizations can analyze user behavior and digital interactions in real time to spot unusual patterns and reduce risks.

There are four main methods of fraud detection:

- Rule-based detection: While helpful for spotting basic irregularities, traditional rule-based detection relies on static thresholds and transaction limits that often fail to catch sophisticated modern fraud schemes.

- Data mining and analytics: Modern analytics engines process vast pools of transaction data in real time to uncover hidden anomalies, such as unusual spending behaviors.

- AI and machine learning: Advanced ML algorithms continuously adapt to evolving threats, using complex neural networks to predict and filter out suspicious actions while keeping legitimate transactions friction-free.

- Biometric and Identity verification: To combat the rapid rise of synthetic identity fraud, organizations deploy advanced biometric tools, facial recognition, and liveness detection to ensure users are exactly who they claim to be.

Reporting and analytics

Financial institutions work with massive amounts of data on a daily basis. Without proper analytics and reporting, the valuable insights such data provides are lacking. With reporting and analytics, stakeholders can see and understand patterns, trends, and insights.

Four key financial statements every software should provide its users are balance sheets, cash flow statements, income statements, and statements of changes in equity. There are plenty of methods, from predictive analytics to prescriptive analytics.

Audit trails

Investopedia identifies the audit trail as a system’s digital paper trail, tracing every single financial data point all the way back to its very first point of origin.

You can think of audit trails as the ultimate source of truth. Companies systematically track accounting ledger entries, trades, etc., to ensure uncompromised transaction transparency. Beyond tracking, audit trails also help flag inconsistencies and block fraud. It ensures that the organization stays aligned with the compliance laws.

Lastly, on a macro level, this strict level of validation keeps the economy stable by ensuring that whenever a company publishes its financial data, the public knows the numbers are 100% real and verifiable.

Role-based access control

In finance, role-based access control is among the industry’s best practices. Beyond security, it prevents insider threats and gives customers and stakeholders a regulatory peace of mind. Additional reasons that prove enforcing role-based control is crucial include:

- Enforcing least privilege: Restricts users’ access to only the data and tools required for their specific job function, preventing unauthorized exposure to sensitive internal systems.

- Reducing admin overhead: Simplifies the onboarding, department changes, and offboarding processes by letting IT admins assign or remove pre-configured roles rather than managing hundreds of individual permissions manually.

- Preventing privilege creep: Eliminates the risk of long-term employees accumulating dangerous, unneeded system permissions over time as they switch projects or roles.

- Meeting compliance laws: Satisfies mandatory regulatory requirements for strict data access control under frameworks like SOC 2, HIPAA, and PCI-DSS.

And lastly, role-based access control limits the potential network damage if a user’s account credentials are stolen or compromised by a cyberattacker.

API integrations

Integrating smartly is how you keep your business on top of the competition while still providing users with a full range of experiences. API integrations are also the backbone of open banking, speed and agility, and accelerated innovation. There are plenty of real-life API integrations that you might encounter daily.

- Payment processing: APIs enable instant and secure payment processing with services like Stripe, PayPal, and Adyen for real-time and cross-border transactions.

- Account aggregation: With user consent, APIs gather financial data from various banks, allowing consumers to have a comprehensive financial overview for better planning and credit assessments.

- Regulatory reporting: APIs facilitate data collection for compliance and regulatory audits, ensuring accuracy and timeliness while minimizing manual work.

- Fraud detection and security monitoring: APIs play a critical role in enhancing security measures against fraud.

Payment processing

The payment processing feature acts as a bridge that connects consumers, merchants, and bank institutions. The key aspects of payment processing include:

- Multi-method acceptance: Support everything from traditional credit/debit cards and direct bank transfers (like ACH, SEPA) to digital wallets (Apple Pay) and instant QR codes.

- Real-time P2P transfers: Give users the ability to send money to friends and family instantly, completely bypassing old-school, multi-day legacy clearing delays.

- Cross-border and multi-currency settlement: Route transactions through global networks so users can seamlessly hold, pay, and receive funds in dozens of currencies with rock-bottom FX markups.

Cloud scalability

Cloud scalability is a system’s ability to dynamically scale its computing power and storage up or down to match real-time user demand.

Instead of guessing hardware needs and overpaying for idle servers, it automatically keeps the app running smoothly during massive traffic spikes and scales back down when things quiet down, ensuring you only pay for what you actually use. In addition to scalability, other benefits of cloud-based financial software include:

- Improving cost efficiency by reducing upfront infrastructure expenses and enabling businesses to pay only for the resources they use.

- The strengthening of data security through advanced protection measures, such as encryption and regular audits.

- These solutions support seamless collaboration and integration by enabling real-time data sharing across teams and systems.

Data backup & disaster recovery

Data backup and recovery refer to the process of creating copies of your data so you can restore it when needed. In the case of financial apps, the data often involves ledgers, transaction records, and client data. Due to strict regulatory compliance, financial institutions rely on automatic, encrypted, and immutable backups.

Having copies of your data is the very first and basic step. Businesses also need to have a recovery plan in place – whether it is granular recovery, instant mass restore, or continuous data protection (which captures and saves data in real time).

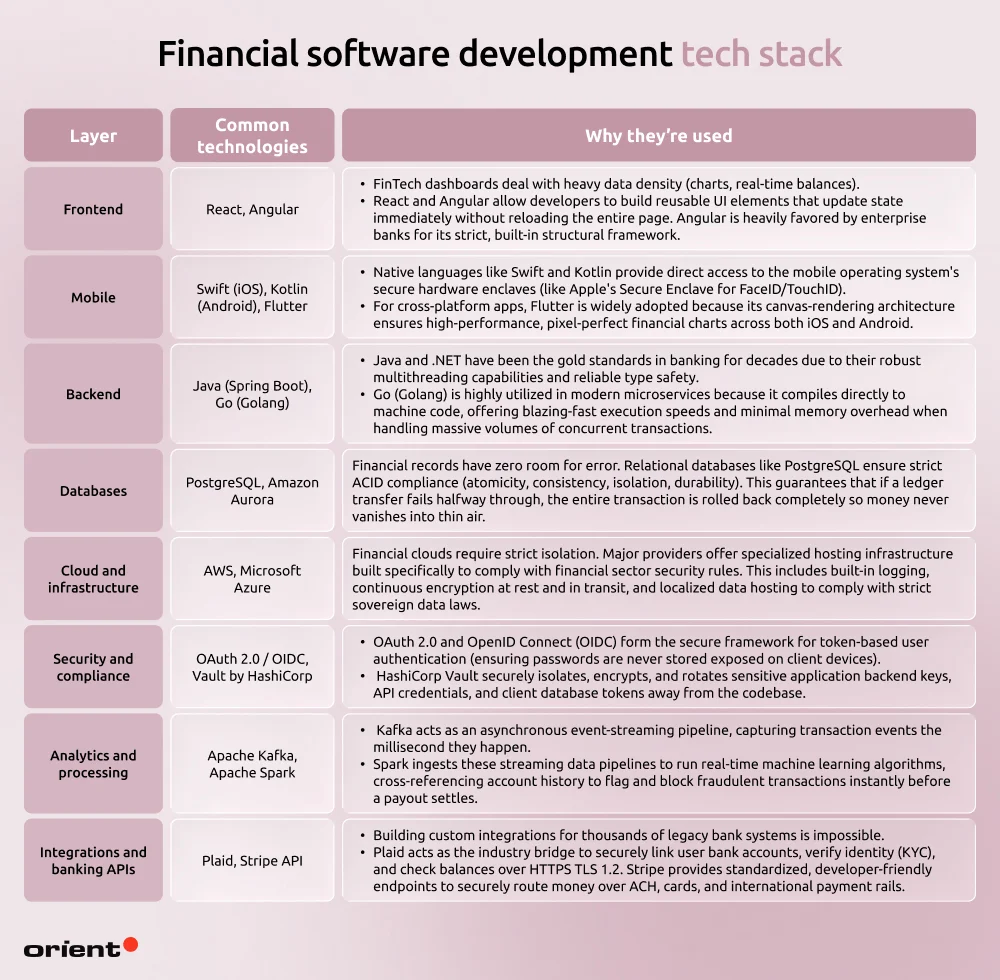

Financial software development tech stack

Choosing the right tech stack can make or break a project. This statement is especially true in financial software apps, where every step and feature is subject to strict regulatory laws. Here is a quick summary of the common technologies used in different layers of financial software.

Financial software development cost breakdown

There is no universal cost range, but based on product type, we can estimate the time it takes to build software and the cost it might take.

| Product type | Estimated timeline | Estimated cost range |

|---|

| MVP fintech app | 2 – 4 months | $60,000 – $150,000 |

| Payment platform | 5 – 12 months | $150,000 – $350,000 |

| Lending software | 6 – 14 months | $150,000 – $400,000 |

| Neobank platform | 9 – 18 months | $180,000 – $500,000+ |

| Enterprise banking system | 12 – 24+ months | $1,000,000 – $5,000,000+ |

Final notes

Compared to other types of software, financial software takes a lot more time and investment in security and regulation requirements. While it does seem overwhelming at first, the payoff is worth it – the finance sector is consistently growing at a two-digit rate. It is a lucrative sector, but companies do need to put enough time and effort into properly developing an app that meets all the security and audit requirements.

The development journey might seem arduous, but you don’t have to do it alone. Let a partner take care of all the compliance requirements and heavy lifting for you – while you focus on actual value-driven activities. Contact Orient Software today and step into the finance world confidently!