Artificial intelligence (AI) has had a dramatic impact on the finance sector, especially when it comes to credit scoring and reporting.

AI credit scoring aims to overcome the limitations of traditional credit scoring by taking into account a potential borrower’s creditworthiness beyond static, historical data points such as their credit utilization and length of credit history.

Find out what AI credit scoring is, how it works, the effect and implications of AI on credit scoring systems, how to incorporate AI credit scoring into a financial strategy, and what to look for in a technology partner offering AI credit scoring solutions.

Key Takeaways:

- AI credit scoring enhances traditional credit evaluation by using machine learning to analyze vast, diverse data sources, offering a more holistic and accurate picture of a borrower’s creditworthiness.

- Expanded financial inclusion: Open access to banking and credit products for under-banked and non-banked individuals by considering alternative data beyond conventional financial records.

- Improved efficiency and fraud prevention: AI-driven models accelerate credit approvals, automate manual risk assessment tasks, and enhance fraud detection by cross-referencing multiple dynamic data sources.

- Continuous learning and adaptability: AI systems evolve over time, identifying new patterns and trends while maintaining fairness, compliance, and scalability through cloud-ready integration with legacy systems.

- Key challenges: Potential data bias, privacy risks, and transparency concerns must be addressed through ethical data handling, clear communication, and explainable AI models.

- Strategic integration: Incorporating AI credit scoring into broader financial strategies helps institutions automate workflows, reduce operational costs, and expand lending opportunities responsibly.

What Are the Limitations of Traditional Credit Scoring?

Traditional credit scoring relies on manually evaluating a potential borrower’s static, historical financial data. This includes, but is not limited to, their credit history length and utilization, proof of income, and debt history.

The limitations of traditional credit scoring are that it doesn’t consider all the factors that determine a potential borrower’s creditworthiness, especially those with minimal or zero credit history. This dis-proportionally affects those who experience difficulties accessing traditional banking services, largely due to regional or socioeconomic circumstances.

An estimated 1.4 billion adults don’t have access to traditional bank accounts, according to the World Bank Group in 2021.

What Is AI Credit Scoring?

AI credit scoring is defined as the process of using advanced AI-powered tools to determine the creditworthiness of a potential borrower.

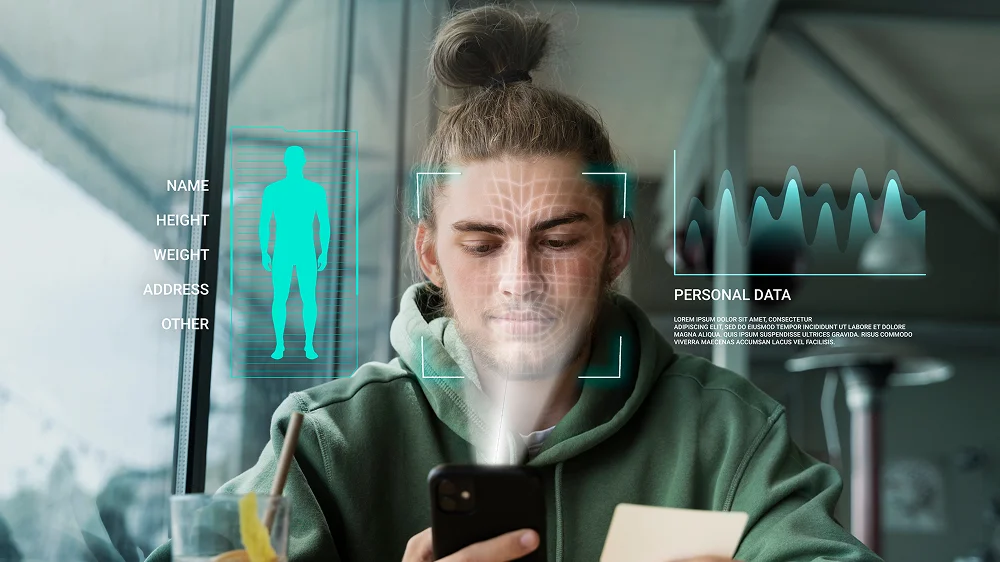

These tools are powered by complex machine learning algorithms that evaluate large amounts of data from unconventional sources, sources that traditional credit scoring methods may miss. Such unconventional sources may include utility bill payments, social media activity, and transactional history from third-party FinTech apps.

By evaluating large amounts of data from vast data sources, AI credit scoring tools can identify trends and patterns and then predict potential future financial behavior. The result is more accurate credit score evaluations, improved access to essential banking services, and higher client satisfaction rates.

How Does AI Credit Scoring Work?

AI credit scoring works by using advanced tools powered by complex algorithms in order to process and analyze data from a wide array of data sources.

By evaluating data sources beyond what traditional credit scoring methods can do, AI credit scoring can more accurately represent an individual’s ability to repay what they wish to borrow – especially those with little to no history with banking services.

The machine learning models that power these AI credit scoring tools are trained on large datasets, which help identify trends and patterns that form an accurate evaluation of one’s creditworthiness. Predictive analytics can uncover subtle nuances that traditional credit scoring methods may miss, even relationships between seemingly unrelated data sources.

Natural language processors (NLPs) can then communicate the findings of an AI-generated credit score in natural, conversational language that humans can understand. This makes it easier for lenders and potential borrowers alike to understand the results generated by the system.

What Are the Advantages of AI Credit Scoring?

When utilized correctly by lenders and other financial institutions, AI credit scoring can help make various financial products – including personal loans and credit cards – more accessible to under-banked or non-banked individuals.

Here are just some of the many advantages of AI credit scoring.

Improved Banking Access for Under-Banked Individuals

Traditional credit scoring methods often leave under-banked individuals, those with limited access to traditional banking services, ineligible for financial products due to their low or non-existent digital footprint when it comes to engaging with banking services.

AI credit scoring helps make banking services more accessible to under-banked individuals by using alternative data sources to evaluate their creditworthiness. Alternative data sources include but are not limited to rental payments, transactions on third-party FinTech apps, and utility bills.

This enables under-banked or non-banking individuals to gain access to essential banking services without having a prior or extensive credit history.

Improved Fraud Detection and Risk Mitigation

Traditional credit scoring methods often miss out on crucial data from unconventional sources. This increases the risk of threat actors successfully carrying out fraudulent and malicious activity, including stealing sensitive personal information and finances or assets.

By cross-referencing data from multiple data sources, including those outside of static, historical data sources, AI credit scoring systems can more easily identify suspicious financial activity. AI credit scoring can also continuously learn from new emerging threats, keeping its threat detection capabilities automatically ahead of the curve.

In partnership with chip manufacturer NVIDIA, American Express uses advanced, long short-term memory (LSTM) models to automatically detect anomalous activity, resulting in a 6% improvement in fraud detection capabilities.

Faster and More Efficient Approval Processes

Traditional credit scoring methods, especially when performed by a lone human assistant, can be slow, time-consuming, and cumbersome. This includes performing tasks like manually reviewing documentation, cross-referencing submission criteria and what has actually been submitted, and requesting modifications.

By utilizing AI-driven credit scoring systems, lenders can more quickly and easily make lending decisions based on real-time data. Instead of spending hours or possibly even days manually reviewing submissions, AI credit scoring systems can approve or deny requests in a matter of minutes or even seconds.

Greater Flexibility and Adaptability

AI credit scoring systems have the potential to continuously learn and improve over time. This helps make the systems faster and more efficient, as well as more adaptable at identifying emerging trends and patterns. This also ensures that credit scoring criteria remain consistently fair and compliant with regional and industry-specific regulations.

Many AI credit scoring systems are cloud-based as well, making them easy to integrate with legacy systems and scale as the financial institution’s needs grow. Technology partners like Orient Software can incorporate modular, cloud-ready AI credit scoring systems into financial institutions with minimal disruption, while retaining the essential capabilities of the existing legacy infrastructure.

What Are the Challenges of AI Credit Scoring?

Despite the many advantages of AI credit scoring, there are challenges to consider. These challenges come in the form of dealing with potential bias in the training data, addressing data privacy concerns, and a lack of transparency in how the AI credit scoring systems work.

With years of experience servicing the financial sector with proven AI solutions, here is how Orient Software overcomes these challenges in fintech app development.

Incorporation of Existing Biases and Unfairness

Machine learning algorithms are only as trustworthy and reliable as the data they’re trained on. Feeding the model insufficient, irrelevant, or outdated data may cause it to make biased or unfair decisions based on the prejudices present in the data.

By inadvertently exacerbating these biases, AI credit scoring systems risk being perceived as unreliable and non-compliant with regulatory standards, reducing their adoption throughout the financial sector.

At Orient Software, we develop, test, and deploy AI models that collect and analyze large, vast data sets from relevant unconventional data sources. The result is more fair and accurate predictions, significantly reducing the risk of potential bias and unfairness in decision-making processes.

Data Privacy Concerns

AI credit scoring systems raise a wide variety of data privacy concerns, including the collection and processing of personally identifiable information (PII).

To operate correctly, AI credit scoring requires a potential borrower’s historical data regarding their financial and borrowing activity. This includes data like bank statements, a history of past financial transactions, loan repayments, and even the frequency of text messages. As a result of having to collect non-regulated data, lenders and financial institutions that deploy AI credit scoring systems must abide by their relevant regional data privacy and security laws.

For places like the European Union, that means abiding by the GDPR (General Data Protection Regulation). Depending on which part of the United States you’re based in, you may be subject to state-specific data privacy laws. For example, California is bound by the CCPA (California Consumer Privacy Act).

At Orient Software, we develop robust, scalable, and secure AI credit scoring solutions that incorporate elements of fairness and transparency into their workflows. We make it easy for financial institutions to collect only relevant data with upfront user consent and compliance with relevant regional laws.

Poor Transparency

AI credit scoring systems are trained on complex machine learning algorithms, which collect and process huge amounts of data from unconventional sources. Due to the complexity of how these systems operate, it can be difficult for lenders and clients to grasp their potential advantages while easing their concerns regarding data privacy and biased decision-making.

For this reason, it’s important that technology partners educate financial partners on how these systems work, and that financial institutions pass on this information to clients in an easily understandable way. Clients have a right to know how such systems calculate their scores and the set of criteria they follow to reach certain conclusions.

One way to improve transparency is to incorporate transparent scorecards into the results. This involves describing what data sources were used to evaluate the data, along with how each data source is weighted against the others.

How to Incorporate AI Credit Scoring into Broader Financial Strategies

AI credit scoring is having a significant impact on how financial institutions evaluate credit risk and approve borrowers.

Generative AI tools like GPT-5, Claude, and Llama possess vast data processing capabilities, strong contextual awareness, and sophisticated reasoning algorithms. This enables them to collect and process large amounts of data and identify trends and patterns that traditional credit scoring methods may miss.

As is the case for generative AI in banking, AI won’t replace bankers but instead will be used as an extension of their existing capabilities. Some of the many ways that AI credit scoring can be incorporated into a broader financial strategy include:

- Enabling lenders to service market segments that were previously closed to them, including under-banked and non-banking individuals with minimal experience using banking services.

- Automating previously manual workflows, such as risk assessment and documentation reviews, thereby reducing underwriting costs and unnecessary manual labor. AI credit scoring also frees up time for lenders to focus on more complex tasks, such as nurturing existing client relationships.

- Incorporating AI credit scoring tools into existing legacy systems, adopting a hybrid approach that leverages the unique capabilities of the AI-driven cloud solution while retaining the core capabilities of the legacy system.

Examples of AI Credit Scoring

Now that you understand what AI credit scoring is and how it works, here are some examples of artificial intelligence in action for the financial sector.

Calculating Loan Interest

By analyzing large amounts of data from unconventional sources, AI credit scoring systems can calculate the estimated interest of a loan for borrowers. They can factor in contributing details, including risk assessment, dynamic pricing, and personalization, tailoring the interest to the individual based on internal and external factors.

Approving Credit Cards and Determining Credit Limits

AI credit scoring systems can be used to determine whether clients have the ability to manage and repay a credit card. It can evaluate dynamic, unstructured data from multiple sources, so as to not just evaluate risk but also determine the optimal credit limit for the individual.

Approving Business Loans

AI has the potential to increase the speed, efficiency, and accuracy of approving complex, large-scale business loans that would otherwise take weeks through traditional means.

While some manual checks and balances are necessary, such as monitoring to rule out money laundering activity, AI credit scoring can help streamline the process of approving business loans.

Choose Orient Software for Your AI Credit Scoring Solution

Orient Software has the skills, knowledge, and experience to incorporate a scalable and secure AI credit scoring system into your business.

By conducting a thorough AI strategy consultation, we can identify opportunities in your existing workflows, where AI-driven solutions can help increase productivity, compliance, and security in your financial institution.

Our enterprise AI solutions help empower agility and fuel innovation, enabling your institution to more effectively service new market segments, minimize risk, and ensure compliance with data privacy laws and regulations.

Contact us today to discover how our AI-driven solutions can empower your financial institution.